A Gift from an IRA

With a gift from your IRA, you have a few options for making a powerful impact.

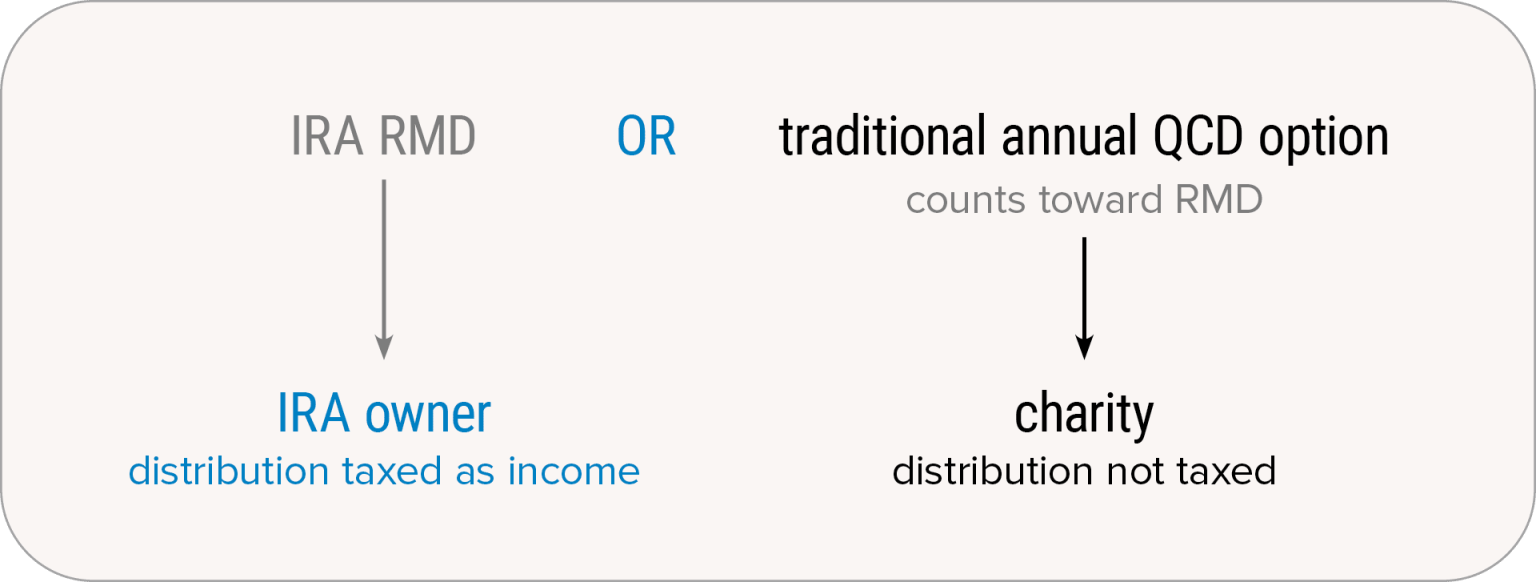

OPTION 1: an outright gift

This is a qualified charitable distribution you can make every year if you wish. You may find it appealing if you would like to make an immediate gift that counts toward your required minimum distribution (RMD). It works like this:

- If you are an IRA owner age 70½ or older, you can direct a transfer from your IRA directly to InterVarsity.

- The gift does not qualify for an income tax deduction, but any amount up to the annual aggregate limit ($111,000 in 2026) is tax free.

- The gift counts toward your RMD if one is due (generally, beginning at age 73).

- Your gift has an immediate impact on reaching students and faculty with the Real Hope of Jesus—and you can make this gift every year if you choose.

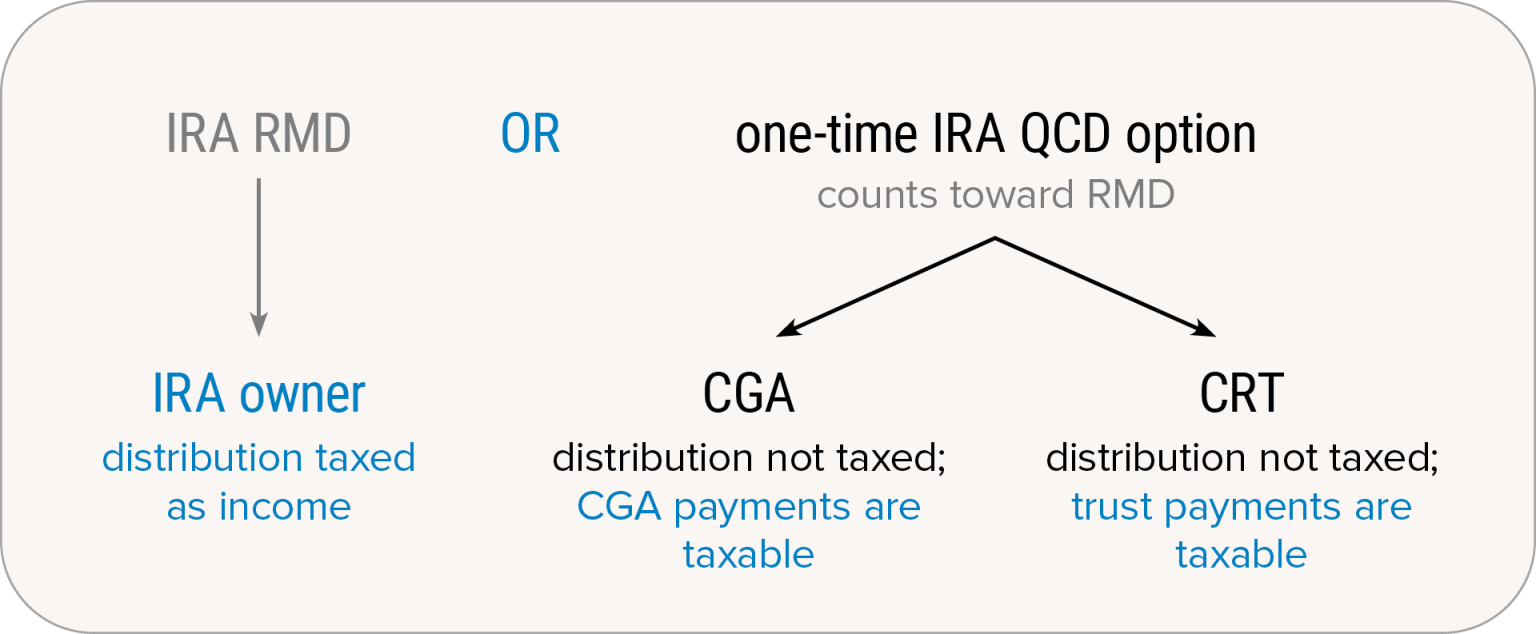

OPTION 2: a life income gift

This one-time qualified charitable distribution lets you make a gift that counts toward your RMD and also creates an income stream for retirement. It works like this:

- If you are an IRA owner age 70½ or older, you can direct a transfer from your IRA to create a new charitable gift annuity (CGA) or charitable remainder trust (CRT).

- The gift does not qualify for an income tax deduction, but any amount up to the limit ($55,000 in 2026) is tax free.

- The gift counts toward your RMD if one is due (generally beginning at age 73).

- Spouses may contribute up to $55,000 each from their own IRAs into a single CRT or a joint-life CGA.

- Income payments may only go to the IRA owner and the owner’s spouse and are taxed at ordinary income tax rates.

- This is not an annual gift—you may only use this option once.

To learn more about these options, click here to read about charitable gift annuities or charitable remainder trusts. Keep in mind that some of the rules and requirements differ if you fund the CGA or CRT from your IRA.

OPTION 3: a charitable beneficiary designation

You may prefer this option if you want to make a comfortable future gift that costs you nothing today. It works like this:

- At any age, ask your IRA custodian for a Change of Beneficiary form.

- You can name InterVarsity as the sole beneficiary or percentage beneficiary.

- You pay nothing now and retain the right to change your gift if your needs and goals change.

- At your death, we will receive the designated assets from your IRA.

Why leave retirement assets to charity?

Retirement account assets left to heirs are highly taxed—once in the estate and again as income to the beneficiaries. Stocks, bonds, mutual funds, and real estate are not subject to income tax when they transfer to heirs. By using IRA assets to make gifts and leaving other assets to family members, you minimize the income tax burden on your heirs, leaving more to your intended beneficiaries while meeting your charitable goals.

Evaluate the fit.

A gift from your IRA may be a particularly good option to consider if you:

- Are an IRA owner age 70½ or older

- Want to avoid paying tax on a required minimum distribution you don't need

- Want to establish a source of fixed income payments to supplement other income streams in retirement

- Are looking for a flexible, easy way to make a significant future gift

See how it works.

Pat, age 75, is required to take a taxable IRA distribution of $15,000 this year. Pat wants to support our work and decides to make a qualified charitable distribution, transferring $15,000 directly from the IRA to us. The transfer counts toward Pat’s RMD, satisfying the distribution requirement, but no tax is due on the distribution. The full amount of the transfer supports our ministry—nothing is lost to taxes!

This year, Sam (age 75) makes a one-time, tax-free QCD of $55,000 to fund a charitable gift annuity with us—an easy way to make a powerful impact on our work drawing students and faculty to Jesus. Sam will receive an annual payment of $3,850 for life, and these payments are taxable each year. If Sam had decided to personally receive the $55,000 distribution this year instead of using it for a QCD, the full amount would have been currently taxable.

Consider your timing.

An outright gift from your IRA can usually be accomplished if you initiate the process in early December. The one-time, life-income option may require a bit more time to set up the CGA or CRT. A beneficiary designation is quick and easy to make at any time.

Making a gift from your IRA

Our Giving from an IRA form will ensure your gift is credited correctly. Please complete and return to direct your gift to the InterVarsity staff member or ministry you want to support. If you have questions, our Estate & Gift Planning team is available to help at (608) 443-3748 or giftplanning@intervarsity.org.

How can we serve you?

We can provide you with more information about any of these options for using your IRA assets to make a gift. You will work directly with your IRA custodian to accomplish these gifts, but please let us know so we can provide substantiation for your qualified charitable distributions. If you make a beneficiary designation, we would like the opportunity to thank you.

We appreciate you including us in your planning.

Making InterVarsity a beneficiary of your IRA qualifies you for membership in our Legacy Fellowship. This is our way to thank you for supporting our future as you plan for yours.